Start for FREE

Start for FREE

Stepping into the accounting field can be confusing at first with all the new terms to learn. Don’t feel left out in conversations, and don’t be left behind only because you aren’t sure what someone is talking about. Learn the basic accounting terms before you start your first big job or before you start your accounting classes, and you’ll be one step ahead of anyone else.

This article is a part of our comprehensive guide – the basic accounting principles for beginners/basic accounting rules. In the article, we have listed essential basic accounting terminologies for beginners. The accounting glossary’s alphabetical layout arrangement will help you look for just what you need to know.

Basic Accounting Terms – [A]

Accounting

Accounting is the process involved in classifying and recording financial data relating to a business. The method includes summarizing, analyzing, and reporting each financial transaction into an accounting system. It indicates completing an accounting year-end, financial statements production, and taxable amount payable by a registered taxpayer.

Accounting Equation

An accounting equation or balance sheet equation defines the fundamental relationship between the assets and liabilities of a business or a person. It is the foundation for the double-entry method of accounting. Under the fundamental accounting equation, each transaction’s total debt is equivalent to total credit.

Asset

Any resource with a monetary value that a business/person owns or controls to benefit from returns shortly. Assets are purchased to bring value and increase the organization’s functionalities or business, thus being recorded in the balance sheet. They are usually listed in the order of liquidity, starting from cash to land.

Basic Accounting Terms – [B]

Balance Sheet

A balance sheet is a timely report that enables business owners and managers to understand the financial statements of assets, equity, liabilities, and capital costs of a business or organization. It falls in line with the accounting equation.

Bank

A bank is a financial institution that securely accepts deposits from the businesses that enable them to pay their bills. Banks provide loans and financial advice to companies directly or indirectly through capital markets aiming to stimulate other businesses’ growth.

Bank Statement

A bank statement is a report of the balance amount in a bank account. It is a periodically issued statement of the holder’s account that entails the amount received and paid out of the bank account.

Banking

Banking is a business activity that includes accepting and safeguarding the money deposited by a person or business. Further, this money is lent out to conduct economic activities to help other individuals or companies succeed or cover operating expenses and investment banks.

Bookkeeper

A bookkeeper is a qualified and trained professional who keeps records of the financial activities of a business.

Bookkeeping Cycle

A bookkeeping cycle is a collective process of accounting procedures such as identification, analyzation, and record-keeping of accounting activities. The usually begins on the 1st of a month and ends on the last day of the month. The cycle repeats every month and is an eight-step process that starts with a transaction and ends as included in the financial statement. The cycle goes on for 12 months until the end of the financial year when entire financial data is sent to a chartered accountant.

Basic Accounting Terms – [C]

Cash Accounting

Cash accounting is one of the accounting methods that records income and expenses when paid for instead of recording when they incur.

Cash Book

A cash book is a financial journal that records all the funds flowing in and out of business through bank accounts. These entries are later updated in the general ledger. The cash book contains all the details of a bank transaction, including the date, amount, transaction description, accounts, and references.

Chart of Accounts (COA)

It is a list of categories of accounts set up in an organizations’ bookkeeping system. The list categorizes the financial transactions that help distinguish the assets, liabilities, income, expenses, and other transactions.

Closing Balance

The ledger account’s final balance comes under the accounts chart at the end of an accounting period or any given day.

Coding

Coding in accounting refers to allocating numbers or letters to accounting data to generate a quick-search database. Coding can vary from one financial organization to another as per their requirements. Thus, coding is not universal and can be tailored to create unique coding systems.

Contra

The Contra account in the general ledger reduces the related account’s value when both are cleared together. The natural balance of the corresponding account is the opposite of that of the linked account. If the debit is the natural balance recorded in the linked account, then the corresponding account registers a credit. In simpler words, if the payment is made to a ledger account, then the same payment is made from the account for some reason, it is called “contra” – the two numbers contradict each other, that is, they cancel each other out of the account.

Commission

The commission is a portion of sales made by a person or company that sells a product owned by another person or company. The owner sets the commission amount as a percentage of the sale proceeds or as a fixed rate, the amount of fixed value. For the seller, it is commission income, and for the owner, it is commission expense.

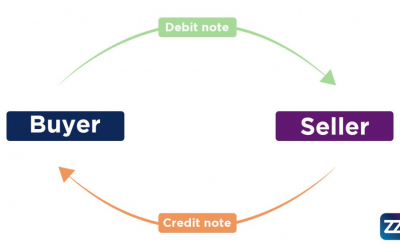

Credit Note

It is a document that provides a refund to the customer for returned or sold goods at an incorrect price.

Creditor

A creditor is a person or company to whom business or an individual owes money for the purchases made.

Basic Accounting Terms – [D]

Data

Data can be defined as the financial information in the accounting system.

Deductible Purchase

A purchase that can be claimed as a business expense is called a deductible expense as it reduces business profits and reduces the amount of income tax owed to the government.

Non-Deductible Purchase

A non-deductible purchase is a purchase that cannot be used to reduce profits and taxes, such as when the owner uses business funds to buy something for personal use.

Double-Entry

An accounting method in which financial transactions are entered twice, once in the debit portion, and once in the credit portion. Always, debts must be equal to credits. If not, the unbalanced statement will have to be balanced by finding the fault or error.

Drawings

Drawing is a term that defines the action of withdrawing money or funds from a business as an owner for personal use.

Basic Accounting Terms – [E]

Expense

Expenses are the cost of operations that a business incurs to generate income. “Making money costs money.” Typical expenses include payments to suppliers, employee salaries, factory leases, and equipment depreciation.

Export Data

It is exporting information to excel or pdf in accounting software for various business purposes. It increases the flexibility of creating reports that saves a lot of time for businesses engaged with many bills.

Export Goods and Services

Exports are goods and services that are manufactured in one country and sold to buyers in another country. Exports, along with imports, constitute international trade.

Basic Accounting Terms – [F]

Fiscal Year

A fiscal year is a one-year time period that companies and governments use for financial reporting and budgeting. The fiscal year is the most basic accounting terms used for accounting purposes for preparing financial statements.

Funds

A fund is a collection of money intended for a specific purpose. These complexes can often be invested and managed professionally. Some of the common types of funds include pension funds, insurance funds, foundations, and grants.

Basic Accounting Terms – [G-I]

General Ledger Accounts

A general ledger account is a record used to order, store, and summarize a company’s transactions. These accounts are arranged in the general ledger (and chart of accounts) with the balance sheet accounts listed first, followed by the income statement accounts.

Income

Income is money that an individual or the company receives, usually in exchange for providing a good or service or capital investment.

Input

Input is data that is entered into a computer for processing. It is the process of entering data into the internal storage of a computer.

Interim Reports

It is an intermediate statement is a financial report that covers less than one year. Interim data is used to convey company performance before the end of regular year-round financial reporting cycles. Unlike annual statements, it is not mandatory to audit interim data.

Basic Accounting Terms – [J-L]

Liability

In financial accounting, liability is known as the future sacrifices of the economic benefits that an entity has to provide to other entities due to past transactions or other past events.

Basic Accounting Terms – [M-N]

Markup

The markup is an increase in the cost of a product to reach the selling price. The price is the seller’s gross margin, which is crucial to pay operating expenses and make a net profit. The amount of markup can be expressed as a percentage.

Nil

Nil signifies the same as zero.

Basic Accounting Terms – [O-Q]

Overhead expenses

Overhead expenses are the expenses related to running a business. It does not include the costs of manufacturing the product or providing the service. For example, overheads often include executives’ salaries and rents.

Payroll

Payroll indicates employee payments made by the employer. Payroll can be a noun when it describes a company’s financial records regarding an employee’s pay. You can also describe payroll as the business process for paying employee salaries and corresponding taxes.

PAYE

Pay-As-You-Earn (PAYE) refers to a system with income tax withholding by employers or an income-based system for paying off student loans.

Petty Cash

It is a small amount of discretionary money in the form of cash used to cover expenses where it is unwise to cash out by check, due to the inconvenience and costs of writing and signing and then cashing the check.

Profit

Earning also called net income, is the number of earnings that exceeds your expenses for your period. In other words, it is the total amount of revenue left after deducting all necessary and equivalent expenses for the period. Please note that I did not reduce all costs that were paid during the period.

Basic Accounting Terms – [R]

Receipt

A receipt is a sheet of a document representing the status of any payment as “paid.” It acts as proof of payment details, which is issued by most of the businesses, by a seller to a receiver after the payment is made in case of a purchase of goods or services, especially when the buyer pays in cash mode. It is essential in business when a transaction is done through cashless mode, debit, credit, and gift cards, as it confirms the precise details of the purchase that help maintain the accounts.

Reconcile

Retaliating or re-assuring any document’s accuracy by another similar detailed document as a reference to overcome the minor errors or dues to be corrected. Especially in account bookkeeping, which involves investigating and fixing the difference by checking the missing details of the documents such as missed invoices or amount to be included to be received, it is known as reconciling.

Recurring

A thing or image that repeatedly occurs periodically over time with the same details as in the first of those is known as recurring actions. In a matter of business, a transaction that repeats itself every week or month regularly with the same amount to be paid or received can be named as recurring/repeating transactions.

Reference

A unique code of combination that is generally used to connect an entity to another utilizing code representing the actual transaction details in search following via journals and ledgers that bookkeeping system follows in business for easy tact of tracing the transactions.

Refund

An amount that is returned to/from a business firm to compensate the extra amount paid in the case or overpay or in point of return of goods is known as a refund. A refund doesn’t need to be in the form of cash during returns.

Basic Accounting Terms – [S]

Single-Entry

An organizing system is adapted by businesses to manage the transaction accounts where the details of the transaction will be entered only once. Only the received or paid details are recorded, which doesn’t utilize ledgers or journals for bookkeeping, known as single-entry.

Software

A set of programmed instructions to make the typing or recording accounting process in business more reliable and error-free is known as software. Examples of software for such tasks include excel and word for typing tasks, Imprezz, Quickbooks, Xero, Sage, MYOB for processing payroll, etc.

Statement

A statement is a professional documentation representing all the financial status of a transaction between two entities as a proof of the commitment. There are various types of statements meant to avail for different departments of finance. Example: Bank statement for representing input and output transaction from a bank account, invoice statement which inputs all the details of the goods and services purchased from a seller, account statement which shows the details of losses and profits gained by the business firm.

Basic Accounting Terms – [T]

Tax (Payroll Tax)

A mandatory collection of tax by an employer from an employee’s salary or wages periodically and is transferred to the governing authorities regularly is known as payroll taxes. A payroll tax is also known as “PAYE” – (Pay As You Earn), a system of collecting income taxes from an employee or a student as a loan repayment.

Tax (Sales Tax)

India’s taxing system imposes taxes on various goods and services, known as sales tax, with varying tax rates from 0% to 28%. These taxes are collected by the seller of the goods from the buyer of the goods or assets at the time of purchase and are paid to the government on an annual or monthly basis. It’s also known as GST, VAT, HST.

Time-billing

Time-billing is an authorized process of collecting, recording, rating daily, or monthly data.

Basic Accounting Terms – [U-Z]

Unpresented

Unpresented term that refers to cheques that are to be deposited to the bank account remains undeposited due to several reasons. It might also be termed as undeposited if the mode of payment is not in cash. It is a commonly used term in banks during the reconciling of the cash accounts.

Wages

Wage defines a fixed rate of the amount that an individual achieves due to the work he/she does on an hourly basis. The worker receives a payment regularly at certain time-interval (monthly, weekly, daily, etc.).

Write-Off

When a buyer delays/holds the unpaid payments, the data is entered into the company’s depths of unsettled funds account. But, when the customer doesn’t have to pay the outstanding due to various reasons, the bookkeeper brings down the customer’s account to zero in the company’s unsettled funds account. This act is known as a write-off.

Conclusion

One of the primary problems that most business owners have to deal with is basic accounting knowledge. You should be familiar with some basic accounting terms, whether you want to hire professionals to manage your books of accounts or for your business accounting. We hope that our comprehensive definition guide has walked you through some of the basic accounting terms that will help.

If you are looking for a pro accounting system to help your small business accounting, check out Imprezz.in, the pioneer of invoicing solutions in India. We offer a 14 days free trial software program for small businesses. Login to know more!

Sign-up for FREE

Sign-up for FREE